Calm Before the Storm?

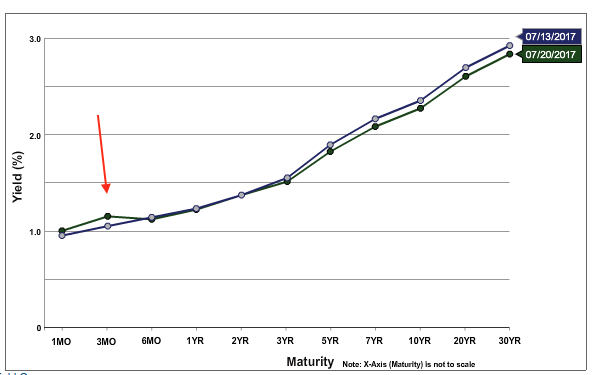

While D.C. is full of fireworks over health care and Russians, the Treasury is scrambling to pay the bills, yet the markets are peacefully awash in Xanax. The spread between the 6-month and 3-month Treasury bills is now pricing in a potential technical default, but given that the rest of the Treasury market looks unaffected, the expectations would be for a quick resolution.

The Treasury yield curve over the past week has adjusted to reflect this pricing. How weird is that to see?

Got to love pricing in a technical default of the U.S. government, not exactly an everyday occurrence, while the VIX has closed below 10 for 6 consecutive days. To put that in perspective, going back to January 1, 1990, the average for the CBOE S&P 500 Volatility Index (VIX) has been 19.5 and the median 17.6. As of yesterday, the average for 2017 has been 11.5 and the median 11.3! In the past 27+ years, the index has fallen below 10 all of 23 times, but 57 percent of those occurrences have been in 2017!

In the past 27+ years, the VIX has fallen below 10 all of 23 times, but 57 percent of those occurrences have been in 2017!

Beware of reversion to the mean.

Treasury volatility is also hitting record lows. Apparently, there is nothing to see here. Thank God it’s Friday.

^CBCB1USTNV data by YCharts