Home No So Sweet Home

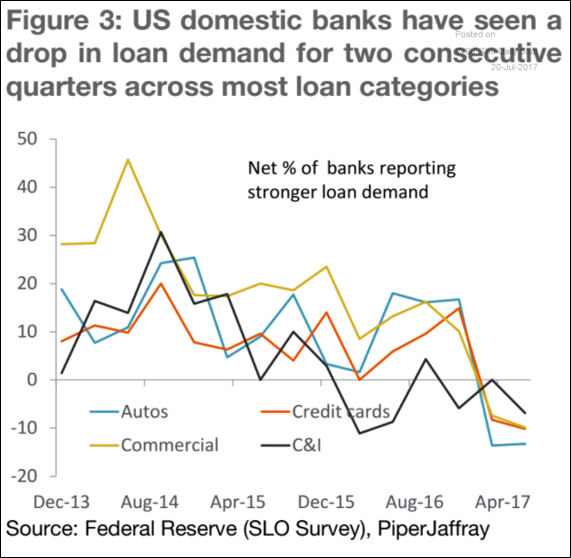

We have written extensively on the pages about weak household spending. As we’ve mentioned before, the only way to increase spending is either through higher incomes or through more borrowing. The borrowing looks to have decidedly peaked.

Wages growth has been weak as well, although yesterday’s quarterly report on median weekly real earnings showed some signs of improving.

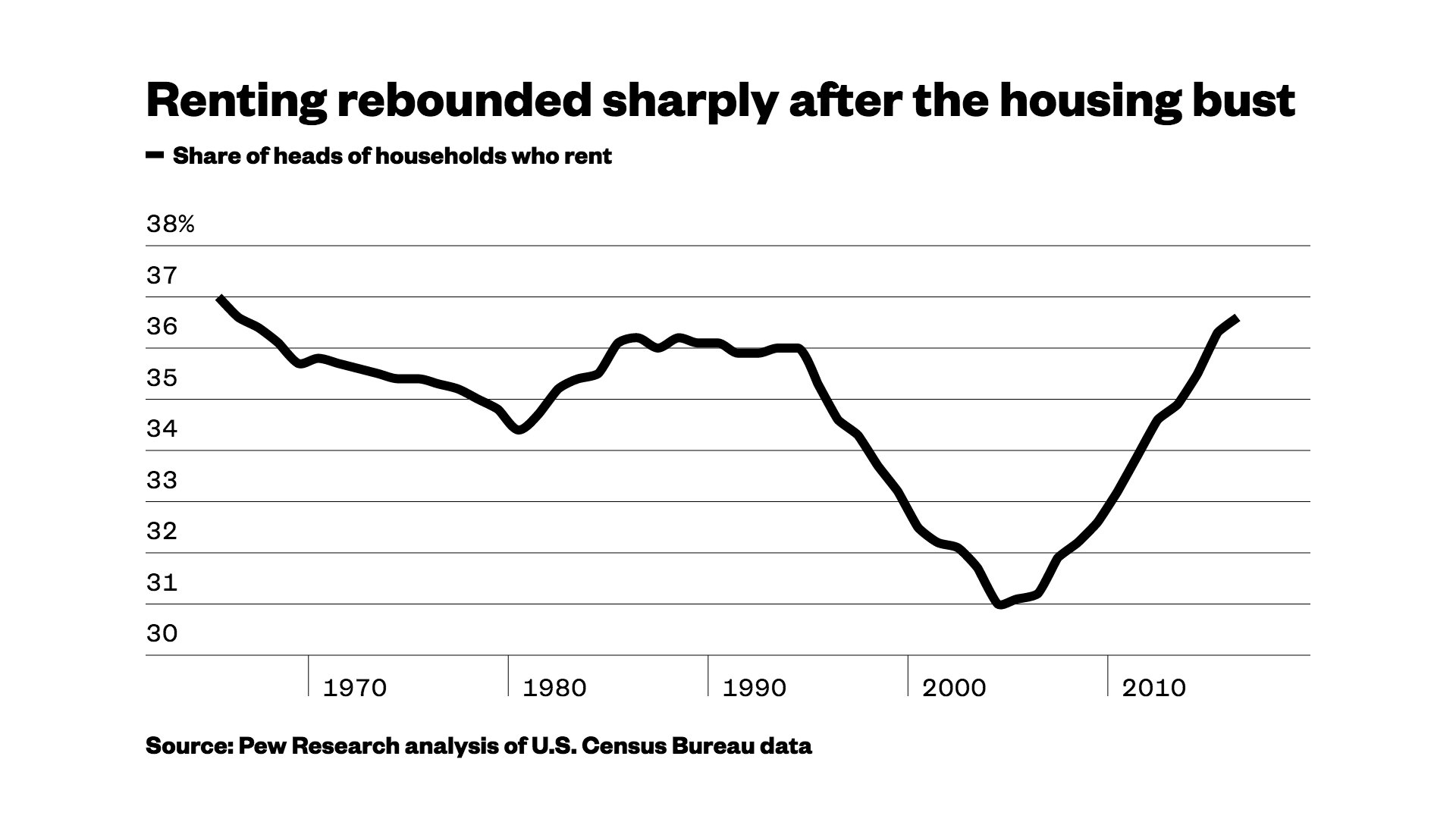

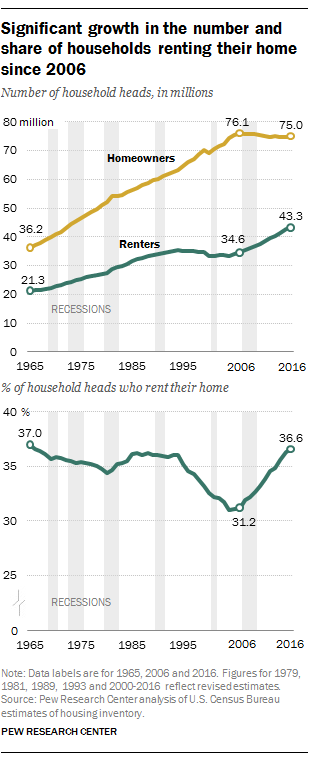

One of the aspects affecting how and where consumers spend is likely related to what we see happening with home ownership versus renting. Home ownership levels are today at levels not seen in many decades.

Instead, consumers are opting to rent.

Over the past 10+ years we’ve seen the number of households that are homeowners decline, while the number of households renting has grown.

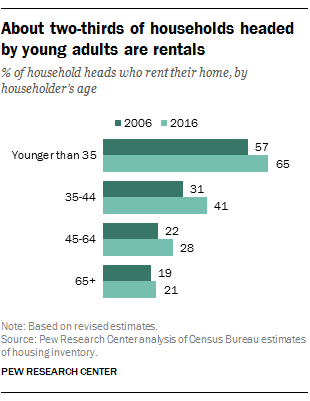

It isn’t just the Millenials either who are preferring to rent versus own.

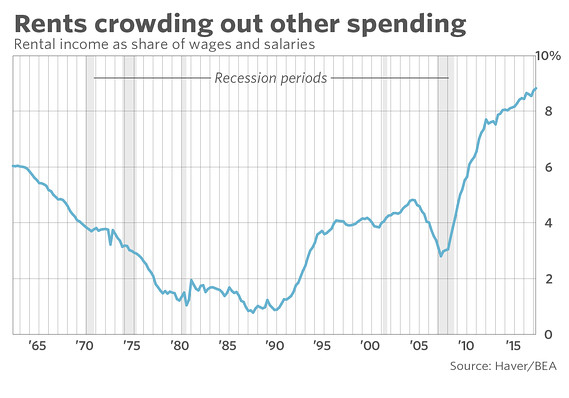

With this rather profound increase in households opting to rent versus own, rising rental rates will have a bigger impact on aggregate spending abilities.

Rental rate increases so far in 2017 are on track to see the biggest gains since 2007, leaving consumers in a tough spot with wages up just 0.8 percent in June while rents are up 3.8 percent on an annualized basis over the past couple of months. Housing costs are having a greater impact on overall inflation than we’ve seen in quite a few years.

While rising rental rates may make buying a home look relatively more attractive, home prices have been rising a much faster rate than wages as the inventory of homes on the market has been at exceptionally low levels. If the Fed is successful in raising longer-term interest rates, the increase in mortgage costs will put home ownership further out of reach for some who may be hesitant to take that risk in the first place.

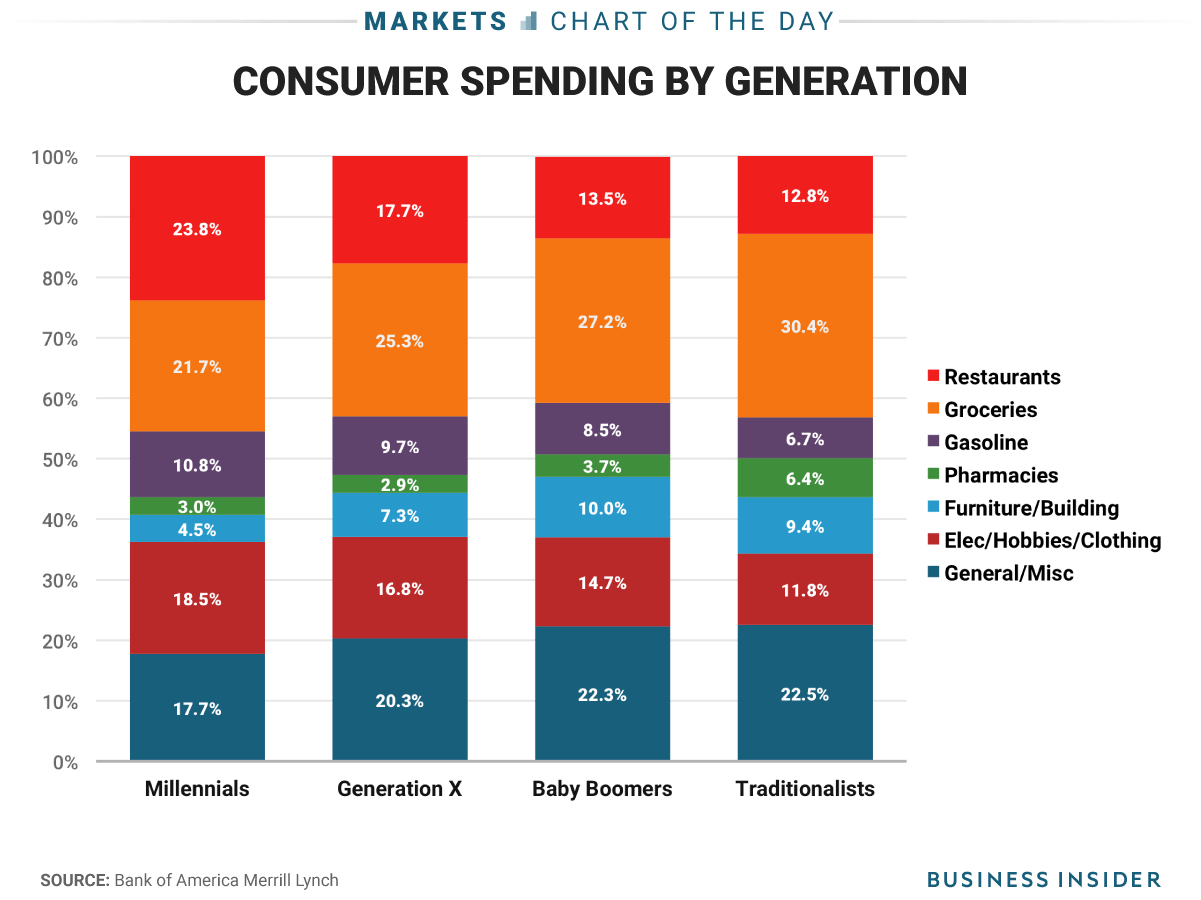

Which brings us to how the various generations choose to spend, with Millennials living up to their reputation by spending a greater portion of their income on restaurants, groceries, technology and clothing.

Bottom Line:

Many consumers still have mortgage/home ownership PTSD after the unprecedented pain felt during the financial crisis. The decades of rising rates of homeownership, induced in large part by federal policies and legislation, has mostly been wiped out. This data illustrates how the generations most affected by the financial crisis have shifted to a more asset-light lifestyle. This shift is a tailwind to those companies providing goods and/or services consistent the sharing economy.